Geographic Indications and International Trade (GIANT)

I. Identification

I. Identification

1. The Issue

Coffee farmers are suffering starvation and social degradation as a result

of the global coffee crisis. Coffee production levels rise while coffee prices

decline. It is not a new phenomenon: commodity producers thoughout history have

lived at the mercy of internationally dependent, volatile markets. Coffee, in

particular, has tended to entice farmers with high prices on the New York exchange

for several years at a time only to crash wehn newly planted trees begin to

bear bountiful harvests--of despair. The latest blut on the market has been

blamed on the caffeinated propulsion of Vietnamese robusta beans onto the market

in the last ten years. However, such an explanation falls far short of accurately

unraveling the international web of factors spawning the global coffee crisis.

While Vietnam has rapidly claimed a commanding presence in the market,

the failure of global cooperative measures among coffee producing and consuming

nations as well as maneuvering by the coffee market's foremost giant, Brazil,

significantly contribute to the global coffee crisis. Coffee farmers from Latin

America to Africa find that they have little reason to harvest their beans.

Drought in Latin America is exacerbating the situation, but participants along

the entire production-consumption chain are wondering which viable solutions

remain.

2. Description

Typically commodities are the most volatile products traded on a global scale

and many of the least developed countries of the world depend wholly on their

export. Coffee is the second most widely traded legal commodity on the international

market, second only to oil. Coffee supports the economies of some fifty producing

countries and garners an average of $55 billion in worldwide sales (Loyd and

Fadel).

The word, "coffee" is derived from the Latin name of the genus Coffea.

The genus is one of 500 genera in the Rubiaceae family and there are 6,000 species

of tropical trees and shrubs within the genera. Of those 25 species are found

in the Coffea genus, all of which are indigenous to tropical Africa and islands

in the Indian Ocean. Coffea species are woody and range from small shrubs to

tall trees over 32 feet in height. The oval fruits usually contain two flat

seeds and are called, cherries. Coffee drinkers are typically interested in

two major and two lesser species within the genus. Specialty (high quality)

coffee is extracted in its pure form from arabica beans of the species Coffea

arabica. Brazilian arabica beans are appropriately known as "Brazils",

while "Other Milds" come from other producing countries where they

grow best at higher elevations. In contrast, robusta beans come from Coffee

canephora var. robusta (Consumers Choice Council, 09/03/01). Robusta implies

more highly caffeinated and bitter beans (P. Tiffen, /10/16/01) that are used

to "make arabica go farther" (CCC 09/03/01). There are many well known

varieties of arabica including: Typica, Bourbon, Caturra, Mundo Novo, Tico,

San Ramon, and Jamaican Blue Mountain grown in Latin America and Jamaica. Robusta

beans however are grown in increasing quantities in West and Central Africa,

throughout Southeast Asia (including Vietnam), and in Brazil where they are

known as Conilon.

Arabica beans represent about 70% of world production, but that is decreasing

as the proportion of robusta beans increases. Robusta trees tend to have higher

yields and are more resistent to disease. Every 3-4 years both arabica and robusta

trees are ready for harvest, and they are viable for 20 to 30 years. Arabica

trees grow better in seasonal climates with a temperature range of 59-75 degreees

Farhenheit; while robust trees prefer warm tropical conditions with more constant

temperatures between 75-85 degrees Fahrenheit. While arabica trees are hardier

in terms of temperature, both species die if exposed to freezing temperatures.

Finally, both need about 60 inches of rainfall annually (CCC 09/03/01).

- Farmers

- Exporters

- Importers

- Roasters

- Retailers

- Consumers

- Certifiers

- Research and advocacy

- Funding groups: The World Bank (WB)

- Trade Associations: Association of Coffee Producing Countries (ACPC), International

Coffee Organization (ICO)

Coffee beans are shipped and warehoused in natural fiber bags, and usually

coffee sales consist of inspected samples offered by importers and brokers (NYBOT

http://www.nybot.com/library/econ.htm 12/17/01). Four multinational corporations

dominate coffee roasting and sales, namely Procter and Gamble Company (Folgers),

Philip Morris Companies Inc. (Maxwell House), Sara Lee Corporation, and Nestle.

Meanwhile Dunkin' Donuts owned by Allied Domecq PLC sells two million cups of

a day--more cups of coffee than any other company in the US (Neuffer 07/29/01).

Such corporations manage to maintain high profits, while coffee farmers and

pickers increasingly receive a smaller and smaller financial remuneration for

their efforts. Proctor and Gamble sells about $1billion in coffee sales annually

through the Folgers brand. While the company has raised millions of dollars

to support education programs, build and remodel schools and donate computers

to schools, they have refused to consider fair trade certification (see Legal

Cluster) (Nolan 10/10/01). In doing so, they are addressing the future needs

of coffee producing communities through education, however frequently, impoverished

people place greater priority on their basic needs such as food and shelter,

which can only be addressed by a systemactic shift in the coffee production

chain.

"Sara Lee is the number-two coffee company worldwide in the roast and

ground segment with brands such as Chock full o'Nuts, Hills Bros. and Superior

in the U.S. and Douwe Egberts in Europe and Uñiao in Brazil."(Sare Lee

Corporation http://www.advisorinsight.com/pub/indexes/500_mi/sle_ir.htm). Starbucks

is also a formidable force but only in the specialty coffee market. It controls

about 1% of the total US market, while dominating the specialty coffee market.

(London 12/03/01) Starbucks and Sara Lee, each offer one Fair Trade blend and

that of Sara Lee's Superior blend is triple certified fair trade, organic and

shade grown.. Meanwhile the big three coffee importers: Folgers, Maxwell House,

and Nestle have not begun to address the more fundamental causes of the on-going

coffee crisis. In addtion, while the specialty market is small in terms of quantity

of beans imported (17% of total US green bean imports) but it does control 40%

of the $18.5 billion US coffee market or $7.8 billion (Giovannucci, 2001: 7).

Starbucks was reported to be having a "blockbuster year" in June 2001,

recording $629 million in sales in the second quarter. But while the green bean

price fell, Starbucks raised its prices (Peraino, 2001). Therefore both the

mainstream and specialty markets are reeping significant benefits from the current

coffee market. The plummeted prices paid to farmers as a result of the New York

exchange market quotes translate into larger profit margins for multinational

corporations. While those multinational corporations may increase their competitive

advantage with socially responsible measures such as education funding, they

are not addressing the fundamental injustice of their profit margins by avoiding

sustainable initiatives such as fair trade, organic and shade grown certification

schemes.

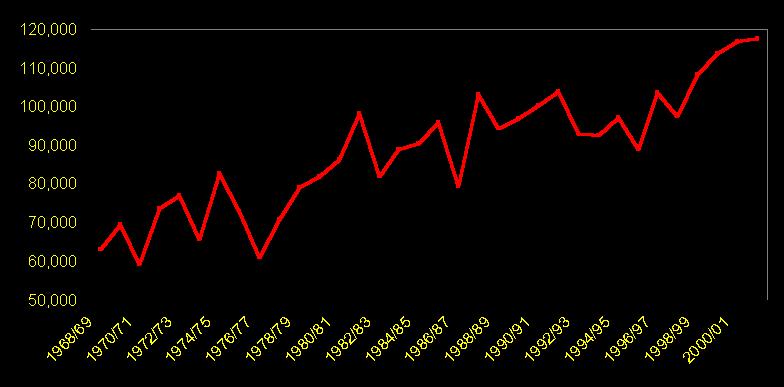

Graph 1: World Coffee Production: 1968-2001

Source: World Bank International Task Force on Commodity

Risk Management in Developing Countries

P. Tiffen & E. Brylla, Nov. 16, 2001

The so-called C-market price (New York commodity exchange market

price) of coffee has been in continual decline over the last several years just

as world production has been increasing steadily (See Graph 1). In 2001, the

New York Board of Trade (NYBOT) C-market price dropped from 60 cents per pound

in December, 2000 to 44 cents per pound in the fall of 2001 (NYBOT). As is true

of most commodities, prices are dependent upon financial speculation and weather.

In 1994, a frost in Brazil created a surge in coffee prices as the world's foremost

producer was unable to supply the same quantity as in previous years (Neuffer)

. Frost and drought are so important

to the international coffee market that the international coffee organization

has included a chart listing them since 1902 (ICO, 12/17/01).

Table 1. Coffee: Exports by ICO Exporting Members (Vietnam) to All Destinations

| October-September |

| (in thousand 60Kg. bags)

1 bag = 137.276 lb. |

|

1994/95 |

1995/96 |

1996/97 |

1997/98 |

1998/99 |

| Vietnam |

3207 |

3679 |

5422 |

6602 |

6558 |

Source: International Coffee Organization, December 1999

Horticultural and Tropical Products Division, FAS/USDA

(Commodity Expert)

Meanwhile, in the last year prices have fallen dramatically as a result of a

glut on the market partially attributed to Vietnamese coffee production. Many

sources cite Vietnam as the sole culprit in the current crisis, "This year,

Vietnam has flooded the market with cheap, low-quality beans, driving prices

to an eight year low." (Neuffer, 2001). Without a doubt, Vietnam has emerged

as one of the most prolific coffee producing countries within the last couple

of decades (See Table 1) and its entrance into the market has created negative

reverberations down the chain of production that are felt by coffee farmers

in countries from all areas

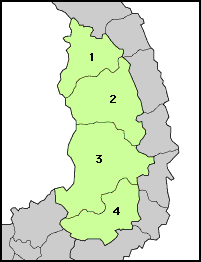

of the world. The central highlands region of Vietnam, namely Gia Lai and Dac

Lac are the two regions where the coffee boom in Vietnam has exploded. Interestingly,

this is also the area in which some of the worst civil unrest in decade's of

Vietnamese history has been taking place (See Other Cluster).

Vietnam

2. Gia Lai

Province

3. Dac Lac

Province

Farmers in Latin America, Africa, and even Vietnam are suffering from the diminishing

wages they receive as a result of the collapsed coffee commodity market. Their

suffering is leading to desperation in many parts of the world. Coffee farmers

typically earn 15 to 25 cents per pound of coffee cherries, which is hardly

enough to cover the cost of production. As a result, many Central American and

Mexican coffee farmers have opted to abandon the labor-intensive coffee industry.

Their decision is having dire effects on the economies of the region as hundreds

of thousands of workers are being displaced. The collapse in coffee prices arrived

at the same time that severe drought and food shortages are plaguing Central

America. Hunger is rampant, the United Nations World Food Program estimates

that up to 1 million Central Americans, primarily in Nicaragua and Honduras,

are going hungry. Coffee farmers whose existence depends on the coffee harvest

being that they do not grow other crops, are especially at risk. (O'Neill, 2001).

In Guatemala a farmer can expect about $8500 before costs for his entire crop

in one year and that same crop will be worth $750,000 by the time it passes

through the numerous hands of the coffee. The President of Guatemala's National

Coffee Association, Manfredo Topke Delgado, states that farmers have no choice

but to offer pickers coffee instead of cash, left the February 2001 crop to

rot on the bushes, and left many farms to the weeds. In Guatemala, coffee production

is a contentious class issue. The landed class owns 3,400 plantations many of

which are "hidden behind high walls and protected by armed guards".

An independent study found that in three of Guatemala's coffee regions, almost

half the workers were paid less than the minimum daily wage of $2.48. But now

the same farmers are likely not being paid at all or are being compensated with

coffee beans. Desperation is running high. In May of 2001, Guatemalan coffee

farmers marched on their capital in Guatemala City to demand cheaper credit

from Congress and offers were made to burn unsold low-grade coffee (Neuffer,

2001) . Some farmers are considering burning the lowest-grade coffee for fuel

or using it for compost, while many in the lowlands are attempting to grow other

cash crops such as bananas palm trees (Franklin, 2001)Topke was quoted in the

Boston Globe in July 2001, "As we see it, we have to compete. The name

of the game is be efficient or you're out. When they ask, are you doing a terrible

job vis a vis laborers, there's not much else that people can do." (Neuffer,

2001).

While prices of coffee reached an eight year low in 2001, the out-migration

of coffee farmers began from the state of Veracruz, Mexico after the harvest

in October and November of the 2000/01 crop. The coffee pickers knew that they

needed to find other alternatives when there was neither cash nor financing

to pay for harvesting and the international prices were progressively decreasing

(Wallgren, 2001). The hopeless situation gained international notoriety when

fourteen Mexicans were found dead of exposure in the Arizonan desert in May

2001, and at least half of  them

were coffee farmers from Veracruz, Mexico searching for alternative means of

survival (McMahon, 2001). According to a Dow Jones Newswire, "Coffee is

an important part of the Veracruz economy," said a local official in Veracruz.

"It's a real bad social problem, and it's sadly not surprising to hear

that many of these immigrants were coffee producers or coffee workers."

. To its credit, Starbucks has been working with Conservation International

in Chiapas, Mexico to expand shade-grown coffee production (See Legal Cluster)

and several fair trade cooperatives have also been established in the same area.

them

were coffee farmers from Veracruz, Mexico searching for alternative means of

survival (McMahon, 2001). According to a Dow Jones Newswire, "Coffee is

an important part of the Veracruz economy," said a local official in Veracruz.

"It's a real bad social problem, and it's sadly not surprising to hear

that many of these immigrants were coffee producers or coffee workers."

. To its credit, Starbucks has been working with Conservation International

in Chiapas, Mexico to expand shade-grown coffee production (See Legal Cluster)

and several fair trade cooperatives have also been established in the same area.

Nicaragua is a case in point. Coffee exports comprise 25% of export revenues

in Nicaragua. 320,000 households get some or part of their income from coffee.

There are 60,000 permanent coffee laborers and 280,00 harvest laborers in the

coffee industry. However, as a result of drought, lack of funding for inputs

and the coffee crisis there was a 30% drop in the coffee yields of the 2000/01

harvest (Tiffen, 2001). The Washington Post reported in Sept. 2001 that coffee

farmers in Nicaragua were literally starving as a result of both a drought and

low coffee prices, which was in turn influencing the political spectrum. As

in Mexico, the situation was encouraging a mass exodus of people (including

coffee farmers) from Nicaragua, Honduras, Guatemala, and El Salvador. According

to a report in the Seattle Post-Intelligencer thousands of Nicaraguans from

coffee plantations were lining the highways with refugee camps where black tarps

serve as their temporary homes. As a result of their desperation, leading up

to the recent elections people were regaining interest in "the Marxist

icon" Daniel Ortega, leader of the Sandinistas during the war-torn decade of the 1980s in Nicaragua

(Jordan). In July 2001, the then President Arnoldo Aleman offered to bus refugees

back to their homes and provide them with jobs building roads and bridges (Mulady,

2001). Few jobs were provided, but nonetheless Ortega conceded defeat in the

elections to his opponent Enrique Bolanos (Aguilar, 2001). Paul Rice, current

Executive Director of Transfair USA, a fair trade certification organization

worked in Nicaragua for 11 years as a rural economic and cooperative development

specialist (Transfair USA website 12/17/01). He stated after a visit to Nicaragua

in 2001, "There were 4000 farm workers who had come down from the big farms.

They hadn't been paid salaries since February. It was a dramatic scene, all

these coffee workers camped out with their families and children." (Mulady,

2001) Thus the ravaged price of coffee on the international markets has deleterious

effects on socio-political aspects of farmers' lives around the world as their

economic disadvantage worsens.

leader of the Sandinistas during the war-torn decade of the 1980s in Nicaragua

(Jordan). In July 2001, the then President Arnoldo Aleman offered to bus refugees

back to their homes and provide them with jobs building roads and bridges (Mulady,

2001). Few jobs were provided, but nonetheless Ortega conceded defeat in the

elections to his opponent Enrique Bolanos (Aguilar, 2001). Paul Rice, current

Executive Director of Transfair USA, a fair trade certification organization

worked in Nicaragua for 11 years as a rural economic and cooperative development

specialist (Transfair USA website 12/17/01). He stated after a visit to Nicaragua

in 2001, "There were 4000 farm workers who had come down from the big farms.

They hadn't been paid salaries since February. It was a dramatic scene, all

these coffee workers camped out with their families and children." (Mulady,

2001) Thus the ravaged price of coffee on the international markets has deleterious

effects on socio-political aspects of farmers' lives around the world as their

economic disadvantage worsens.

In Africa, where 39 of the world's 49 poorest countries are located, the global

coffee crisis has increased poverty. Many countries in Africa rely heavily on

coffee as a source of foreign exchange earnings. In March 2001, a conference

was held in Nairobi, Kenya at which the ICO Chief Economist stated that African

coffee industry needs aid because it is increasingly loosing its share of the

market. While Africa controlled 27% of the world market in the 1980s with an

average of 26 million bags, it is averaging 17 million bags or 15% of the current

market. Declining farm incomes may be leading to lower investment in harvesting

as farmers employ fewer workingmen to pick cherries. While cherries are seen

"drying by the side of the road in some areas, many farms remain unharvested

and overrun with weeds." (OT Africa Line, 2001)

Uganda is highly dependent on the coffee industry. coffee exports account for

47% of its export earnings. Nearly 2.5 million people are involved in coffee

production, making the industry the largest employer of hired labor. Liberalization

of the Ugandan economy and the coffee industry has lead to greater price volatility

internally, which has lead to suffering at the household level and the financial

services level as banks struggle to survive. As a result credit for domestic

companies and local cooperatives has significantly faltered. (Tiffen, 2001)

Low coffee prices and thus lower production is further immiserating Africans

across the continent dependent on coffee farming.

(See Other Cluster for Vietnam specific social implications as well as Colombia

)

Coffee production on large plantations typically involves the deforestation

of large tracts of land. In addition, the processing of coffee beans can require

the use of large quantities of water into which organic coffee waste is dumped.

Deforestation can cause soil erosion, lower biodiversity by destroying the habitat

of countless living species, and significantly limit carbon sequestration due

to the loss of dense forest that tends to absorb large quantities of carbon.

While there is little research about the direct effect increased coffee production

in Vietnam is having on the environment, many lessons can be learned from research

conducted in Latin America. Tropical rainforest destruction continues throughout

Central and South America as farmers clear-cut hillsides and fields to grow

coffee with greater sun exposure. Coffee tends to grow faster with more sun

but also requires more pesticides. The pesticides affect the growers more severely

than the consumers since processing removes most of the chemicals. However,

the end result is that the prevalence of pesticide use on large plantations

worsens the social implications in producing countries of the present coffee

market. In addition, the Smithsonian Institution has lead research into the

effect that clear-cutting for sun-grown coffee has had on migratory birds that

winter in the Mesoamerican Biological Corridor of Latin America. This area of

high of extremely rich biodiversity is the traditional habitat for the wintering

birds, but as it is destroyed the birds are deleteriously affected as are numerous

mammals and reptiles (CEC 1999). (McMahon, 2001)

The global environmental implications of coffee production are strikingly described

in the following exerpt from Stuff the Secret Lives of Everyday Things by

John C. Ryan and Alan Thein Durning:

Dense manicured rows of Coffea arabica trees covered the

farm, growing under the strong tropical sun. For most of this century, coffee

grew on this farm in the shade of taller fruit and hardwood trees, whose canopies

harbored numerous birds, from keel-billed toucans to Canada warblers. In the

1980s, farm owners sawed down most of the shade trees and planted high-yielding

varieties of coffee. This change increased their harvests. It also increased

soil erosion and decimated birds, including wintering songbirds that breed

near my home. Biologists report finding just 5 percent as many bird species

in these new, sunny coffee fields as in the traditional shaded coffee plantations

they replaced.

With the habitats of birds and other insect eaters removed,

pests proliferated and coffee growers stepped up their pesticide use. Farmworkers

wearing shorts, T-shirts and sloshing backpacks sprayed my tree with several

doses of pesticides synthesized in Germany's Rhine River Valley. Some of the

chemicals entered the farmworkers' lungs; others washed or wafted away, only

to be absorbed by plants and animals.

Workers earning less than a dollar a day picked my coffee

berries by hand and fed them into a diesel-powered crusher, which removed

the beans from the pulpy berries that encased them. The pulp was dumped inot

the Cauca River. The beans, dried under the sun, traveled to New Orleans on

a ship in a 132-pound bag. For each pound of beans, about two pounds of pulp

had been dumped into the river. As the pulp decomposed, it consumed oxygen

needed by fish in the river. (1997)

What can be done to raise coffee prices on the international commodities market?

How can the vacillating pattern of coffee prices be normalized? What historical

lessons can be used to better the next steps taken? And what international measures

are needed in order to ensure that more of the profits of relatively inelastic

demand for coffee in the richest countries of the world is shared with the people

who grow and pick the coffee beans? The international coffee market has a long

history of price volatility. Throughout the years greater price stability was

sought through many techniques. Today, perhaps the failed International Coffee

Agreements can be re-visited. Concerted efforts by producing countries to withhold

low-grade or triage beans, burn such stock or use it for compost, fodder or

fuel might be considered. International commodity risk measures such as price

insurance through local and international institutions may present solutions.

Finally, sustainable coffee initiatives provide viable models of coffee production

that are both socially and environmentally sound while involving support from

not only producer but also consumer stakeholders.

3. Related Cases

Cases:

Key words:

- Coffee

- Vietnam

- Southern North America

4. Author and Date:

Janine Johnston, December 2001

II. Trade

Clusters

12. Type of Measure: Quotas

imposed by International Coffee Commodity Agreements (the last one was suspended

in July 1989).

- Regulatory standard [REGSTD] intended to curb oversupply

13. Direct v. Indirect Impacts:

Indirect [IND]

14. Relation of Trade Measure to Environmental

Impact (See Description Cluster: "Global Environmental Implications

Section")

a. Directly Related to Product: Yes

b. Indirectly Related to Product: No

c. Not Related to Product: No

d. Related to Process: Yes, habitat loss and

labor force implications

15. Trade Product Identification:

Coffee

16. Economic Data

17. Impact of Trade Restriction:

Low

18. Industry Sector: [N]

[FOOD]

19. Exporters and Importers:

Vietnam and Various (US, EU,

International Coffee Organization

Statistics

Vietnamese Coffee Exports and The World c-Market Price for Coffee

The propulsion of Vietnam begun after 1980. In that year Vietnam exported 8,000

tons of coffee (with a yield of 0.4tons/ha), while in 1994 its exports rose

to 430,000 tons (with a yield of 2.26 tons/ha) (UNDP legal cluster). Between

1990 and 2001 coffee production shot up from 1% of world production to 18% (Procafe,

2001). Similarly, between 1990 and 1999 merchandise exports from Vietnam rose

from $2,404 million in 1990 to $11,523 million in 1999. Vietnam has three key

competitive advantages: labor, land and finances. However coffee production

is having negative consequences on the labor force and land of Vietnam as is

true of many parts of the world (see Enviromental and Other Clusters).

As stated previously, the World Bank has been implicated in the propulsion

of the Vietnamese coffee market over the last decade. But the World Bank contends

that its lending policies have little or nothing to do with the coffee situation

in Vietnam and thus the world.

While the World Bank has a large and very succesful lending

program in Vietnama for projects covering human development...none of its

investmens have been designed promote coffee production--this contradicts

a number of media reports suggesting that the World Bank has been involved

in financing the massive expansion of coffee production in Vietnam, leading

to a decrease in global coffee prices.

Coffee's main supporter in Vietnam is the Government, through

a large state-owned enterprise and several provincial governments, notably

in the Central Highlands, which have boosted Vietnam's coffee output from

less than 6 million bags in 1997 to more than 12 million bags in 2001 rendering

it the second largest coffee exporter after Brazil. Expansion is also fueled

by small-scale producers going into coffee production on their own with very

little information or experience of world commodity markets. The major expansion

of coffee production in Vietnam started long before the World Bank resumed

lending to the country in 1994. (World Bank, 2001)

It is credible that the Bank had little to do with funding Vietnam's development

of its coffee market. Perhaps the Government saw an opportunity at a time when

the market was high, as many others have done, and opted to gear its command-driven

policies toward the efficient expansion of the coffee market. While the coffee

producing countries are in dire straits and part of the blame lies with Vietnam,

it is not the sole culprit, nor does it hold the panacea. See the Legal Cluster

for possible internationally engaging solutions.

Meanwhile, a closer look at the trade aspects of the coffee commodity market follows.

The graph below demonstrates the volatility of coffee prices from 1983 until 2001.

One can see the steady decline over the last seven years and the new lows to which

the prices have fallen.

Graph 2. Coffee Prices: 1983-2001

Source: World Bank International Task Force on Commodity

Risk Management in Developing Countries

P. Tiffen & E. Brylla, Nov. 16, 2001

The average price of coffee from 1994 to the present as estimated from the

NYBOT Interactive Historical Chart below. (See Chart

Chart Average Coffee Price from 1994/95 to 2000/01

| Average Price on New York Bureau of Trade in $US

($/100lb.) |

| 1994/95 |

1995/96 |

1996/97 |

1997/98 |

1998/99 |

1999/2000 |

2000/01 |

To date |

| 166 |

136 |

121 |

226 |

104 |

87 |

73 |

55 |

Source: NYBOT Trade Signals Historical Interactive Chart

KC NYBOT Contin. (Monthly) 10 years

Compare the average coffee prices above with the fluctuations in production

since 1994/95 below in Graph 3.

Graph 3. Production Changes Worldwide Since 1994/95 (USDA Data)

Source: World Bank International Task Force on Commodity

Risk Management in Developing Countries

P. Tiffen & E. Brylla, Nov. 16, 2001

Since 1997 there has been a continuous and steady decline in the price of coffee

on the international commodity market. In Graph 2 one can see that the average

price has decreased substantially over the last five years. The coffee year

begins October 1 and ends September 1 (International Coffee Agreement 1994).

Thus, despite the halt of trading due to the bombing of the World Trade Center

on September 11, 2001 has seen the lowest price for coffee within the last ten

years.

. In 2000, Vietnam produced 450,000 tonnes of robusta beans. While in many

parts of the world, specifically Colombia and Indonesia which were negatively

affected by El Nino and La Nina phenomena, the coffee output in 1999/00 declined

(FAO). Although the robusta market is considerably smaller than the arabica,

prices and the quality of robusta is much lower than arabica, the glut of Robusta

beans affects the overall c-market price.

While production worldwide declined (although it increased in Viet Nam and

a few other producing countries) coffee trade expanded in 1999/00 (FAO). Overall,

world exports in green bean coffee were greater than 5.1 million tones, almost

14 percent greater than the average for 1995-97. Vietnam exports were 270 tonnes

between 1995-97 and 464 tonnes in 1999(FAO). Similarly, as seen in Table 1 above

Vietnam exported an average of 3,207 60 kilogram bags of coffee in 1994/95,

which rose to 6,558 60 kilogram bags by 1999/00(USDA).

Comparisons of Coffee Exporters and Importers

Leading Exporters Quantity of 60 kg. bags: (See Table Below)

Brazil is by far the number one exporter of coffee beans both arabica and robusta.

It has fairly consistently out performed all other producing countries. In 1998/99

it exported a record 22,771,000 60kg bags of coffee. Traditionally, Colombia,

land of Juan Valdez, has followed Brazil as the second most abundant producing

country. However, what is not shown on the Table 3 below is that in 2000/01

Vietnam overtook Colombia as the second most prolific coffee producer and was

the number one producer of robusta beans in that same harvest year. During the

calendar year of 2000 Vietnam produced 11, 177,885 60 kg. bags of coffee (Commodity

Expert 17/05/01).

Table 3. The Top Ten Exporters

Coffee: Exports by ICO Exporting Members to All Destinations

| October-September |

|

(In thousand 60-Kg. bags) 1 bag

= 132.276 lb.

|

| Country |

1994/95 |

1995/96 |

1996/97 |

1997/98 |

1998/99 |

| Brazil |

16544 |

12728 |

18627 |

16325 |

22771 |

| Colombia |

9342 |

10785 |

11176 |

10911 |

10291 |

| Vietnam |

3207 |

3679 |

5422 |

6602 |

6558 |

| Indonesia |

3143 |

6098 |

6358 |

5367 |

5417 |

| Guatemala |

3564 |

3713 |

4224 |

3889 |

4557 |

| Mexico |

3258 |

4579 |

4389 |

3883 |

4136 |

| Uganda |

2793 |

4214 |

4237 |

3032 |

3648 |

| India |

2070 |

3572 |

2476 |

3691 |

3568 |

| Cote d'Ivoire |

2253 |

2900 |

3574 |

4567 |

2705 |

| Honduras |

1637 |

2054 |

1825 |

2299 |

2087 |

Source: International Coffee Organization, December 1999

Horticultural and Tropical Products Division FAS/USDA

(Commodity Expert 13/12/99)

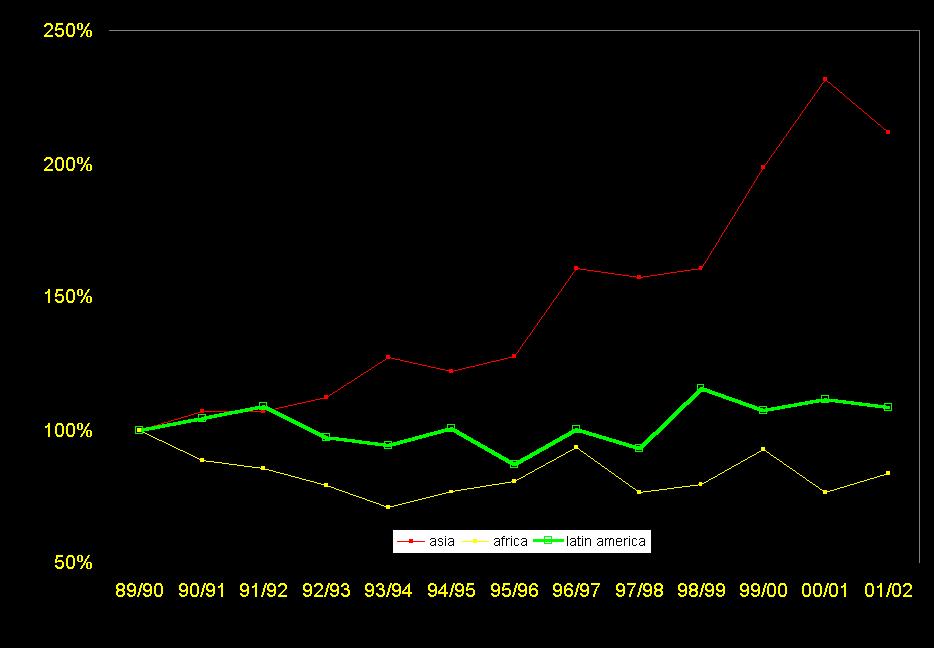

Below in Graph 4. is a depiction of the regional changes in production

Graph 4. Regional Changes in Production

Source: World Bank International Task Force on Commodity

Risk Management in Developing Countries

P. Tiffen & E. Brylla, Nov. 16, 2001

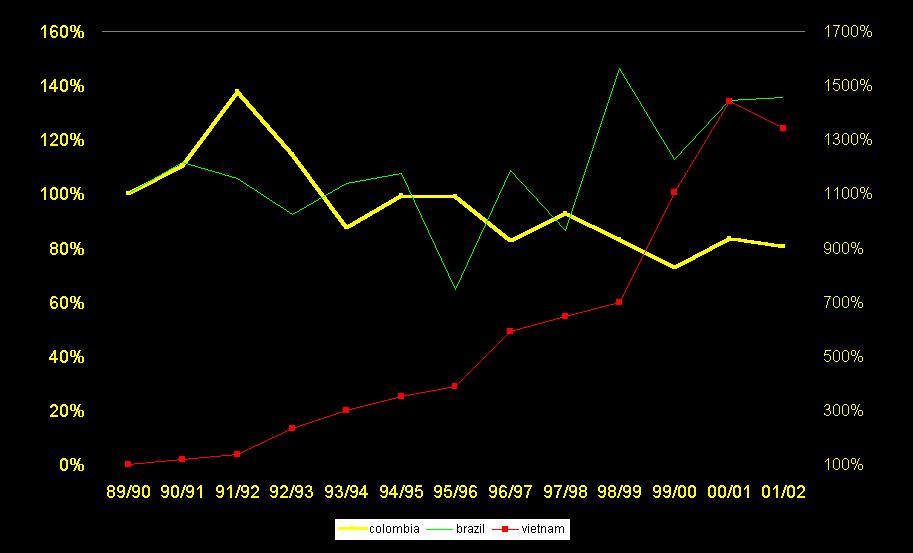

The regional changes in Graph 5. are mirrored by the production

changes in the largest three producers as seen below in Graph

Graph 5. Production Changes in Largest Three Producers

Source: World Bank International Task Force on Commodity

Risk Management in Developing Countries

P. Tiffen & E. Brylla, Nov. 16, 2001

Case Importers :

USA, Germany, Japan, France, Italy, Spain, Canada, UK, Poland, Netherlands

Leading Importers Quantity of 60 kg. bags: (See Table Below)

The United States is the number one importer of coffee in the world. In recent

years the specialty coffee market is the only portion of the market that is

consistently growing but it is growing by 5-10% per year (Giovannucci, 2001).

Germany is the second largest importer of coffee and Japan the third largest.

(See Table 4.)

Table 4. The Top Ten Importers of Coffee

USDA: World Coffee Consumption by Importing Countries

| October-September |

|

(In thousand 60-Kg. bags) 1 bag

= 132.276 lb.

|

| Country |

1994 |

1995 |

1996 |

1997 |

1998 |

| USA |

17326 |

17363 |

18049 |

17771 |

19204 |

| Germany |

10214 |

10032 |

9777 |

9870 |

10375 |

| Japan |

6089 |

6224 |

5922 |

6095 |

6343 |

| France |

5112 |

5313 |

5531 |

5550 |

5437 |

| Italy |

4768 |

4639 |

4731 |

4866 |

4936 |

| Spain |

2791 |

2749 |

2941 |

3035 |

3385 |

| United Kingdom |

2640 |

2200 |

2380 |

2419 |

2241 |

| Canada |

2407 |

2109 |

2291 |

2229 |

|

| Netherlands |

2122 |

2293 |

2548 |

2390 |

1631 |

| Poland |

1832 |

1728 |

1851 |

2192 |

|

Source: International Coffee Organization, December 2000

Horticultural and Tropical Products Division, FAS/USDA

A comparison of human development to economic development:

Human Development and Economic Indicators for Top Ten Coffee Exporting Countries

| |

|

|

|

| |

HDI Value

|

GNP/cap

|

GDP Index

|

|

Country

|

1994, 1997

|

1995 $

|

1997

|

| Brazil |

0.783, 0.739

|

3640

|

0.70

|

| Colombia |

0.768

|

1910

|

0.70

|

| Vietnam |

0.557, 0.664

|

240

|

0.47

|

| Indonesia |

0.668, 0.681

|

980

|

0.59

|

| Guatemala |

0.572, 0.624

|

1340

|

0.62

|

| Mexico |

0.786

|

3380

|

0.74

|

| Uganda |

0.404

|

240

|

0.41

|

| India |

0.544

|

340

|

0.47

|

| Cote d'Ivoire |

0.422

|

660

|

0.42

|

| Honduras |

0.575, 0.641

|

600

|

0.52

|

Sources: Human Development Report 1999

World Development Report 1997

Interestingly, the human development index as well as the GNP and GDP of the

top ten coffee exporters are not comparable with the degree to which they export

coffee. Although Viet Nam is becoming a major exporter of coffee it has a very

low GDP/GNP in the years cited.

III. Legal

Clusters

5. Discourse and Status:

The socially and environmentally unsustainable imbalance

created by the current international coffee market clearly necessitates a new

system of exchange. There are several possibilities:

- International Coffee Agreements (ICAs)

- Producer Price Stabilization Schemes

- Oversupply Controls

- Product Differentiation

- Sustainable Coffees (Fair Trade, Organic and Shade

Grown)

The first International Coffee Agreement was signed in 1962. It was a five

year agreement meant to fix export quotas in coffee producing countries in order

to stop the extended decline of prices. The agreement was renewed every five

years until 1989 when the final agreement expired. In that year the Association

of Coffee Producing Countries (ACPC) was established to create a quota system

designed to maintain prices.

The International Coffee Agreement 1994 in turn established the International

Coffee Organization, a multilateral organization of equal representation between

producing and consuming countries was initiated with the following objectives

according to Article I of the Agreement:

1. to ensure enhanced international cooperation in connection with world

coffee matters;

2. to provide a forum for intergovernmental consultations, and negotiations

when appropriate, on coffee matters and on ways to achieve a reasonable balance

between world supply and demand on a basis which will assure adequate supplies

of coffee at fair prices to consumers and markets for coffee at remunerative

prices to producers, and which will be conducive to long-term equilibrium

between production and consumption;

3. to facilitate the expansion of international trade in coffee through the

collection, analysis and dissemination of statistics and the publication of

indicator and other market prices and thereby to enhance transparency in the

world coffee economy;

4. to act as a centre for the collection, exchange and publication of economic

and technical information on coffee;

5. to promote studies and surveys in the field of coffee; and

6. to encourage and increase the consumption of coffee. (International Coffee

Agreement 1994)

This agreement was renewed for two years November 23, 1999 (The Council of

the European Union). Within the last year coffee producing countries have agreed

to reduce the role of the ACPC as a result of the impotence of coffee retention

measures it implemented and to strengthen the role that the ICO will take in

harmonizing consumer-producer relations in order to stabilize the market (Commodity

Expert 25/09/01). In addition, while the World Bank and IMF have been implicated

as accomplices to the initiation of the current dismal state of coffee prices

as a result of loans they extended to Viet Nam, ironically ACPC members are

now discussing a plan to request that the World Bank get involved in a program

to reduce worldwide production temporarily in order to boost prices. This measure

is being considered despite the fact that Brazil's Agriculture Minister Marcus

Vinicius Pratini de Moraes was quoted in the Brazilian press during the first

week of August 2001 stating,

"Coffee is experiencing problems because the World Bank and the French

government have financed Vietnam, throwing onto the market 15 million bags without

any controls. It is unacceptable for the World Bank to do this…there is

no retention programme which can turn the situation around."

What Minister Pratini de Moraes did not recognize is the strength of the Brazilian

market share. He did not mention the fact that Brazil is currently moving most

of its plantations to lowland areas where production can become more mechanized.

It is less susceptible to frost in such areas but more prone to effects of drought.

However, irrigation systems can allay drought damage, thereby fortifying Brazil's

vice-like grip on the coffee market.(Tiffen, 2001)

Several reasons have been identified for the failure of the agreements. As

more countries are embracing liberalized trade at the policy level as promoted

by developed countries, the agreements are seen as barriers to free trade. Consuming

countries must support the intiatives by demanding certificates of origin in

order to enforce the quotas (but they will fail to do so if they view an ICA

as inhibitive to liberalized trade) (Hamrlik, 2001: 59). Also commodities agreements

over a commodity market that is dominated by a few producing countries (as is

the case with coffee in relation to Brazil and Colombia, traditionally) tend

to fail if the controlling countries choose not to participate (Coote, 1996).

Brazil has been implicated for failing to uphold the agreements. Brazil's relative

power in the industry also explains the failure to develop a coffee cartel,

as a cartel necessitates fairly equally powerful producing members. While it

is too early to say whether Vietnam would follow Brazil's lead or perhaps serve

to balance Brazil's lop-sided control of power in the coffee industry, Vietnam

did attempt to adhere to oversupply agreements as discussed below (see Oversupply

Controls.)

Producer Price Stabilization Schemes

The World Bank is working on an international task force to devise commodity

risk management measures. They are proposing a price stabilization plan that

would involve price insurance negotiated through local institutions from banks

to local cooperatives. A minimum price would be offered to producers who are

generally excluded from access to such market-based solutions such as price

insurance. The Bank plans to identify the local institutions that may have the

greatest efficacy at reaching the farmers who are most in need of such mechanisms

and then to develop a broad-based strategy to deliver the needed financial support

to them. The primary objective of the scheme is bridging the market gap between

providers of risk management instruments and small farmers in developing countries.

In the terminology of the World Bank, the International Task Force on Commodity

Risk Management in developing countries approach is as follows:

- Identify risks and who carry the risks

- Identify “Local Transmission Mechanisms”, or LTM’s (eg, cooperatives,

banks, constriction points in the marketing chain)

- Identify market-based instruments that could be made available to LTMs and

which would address the identified risks.

- Build capacity in the LTM to use these instruments, and transmit their benefits

to farmers.

- Ensure ability of the LTM to access the international market for these instruments.

(Tiffen, 2001)

Pilot projects are being carried out in Nicaragua, Tanzania and Uganda. However,

this is a relatively new initiative that has yet to prove its viability. Only

time will tell whether such a broad-based approach is feasible and which aspects

of it are more so than others.

Oversupply Controls

Before its dissolution in the fall of 2001 the Association of Coffee Producing

Countries (ACPC) in accordance with the ICO were suggesting means of curbing

the oversupply of coffee through a global coffee retention scheme. By September

2001 there was a general agreement to slowly release the retained stocks, the

quantity of which was not known. From Colombia to Costa Rica to Indonesia to

Vietnam and back to Brazil, countries chose to begin releasing their stocks.

Vietnam released the 2.5 million bags it had retained between November 2000

and mid-August 2001 by mid-September (Commodity Expert 25/09/01). Colombia,

Mexico, Costa Rica, El Salvador, Honduras, and Nicaragua all participated in

the retention scheme and asserted their interest in supporting another proposal

to limit the exportation of so-called triage or low quality arabica beans. However,

Vietnam is not a member of the ACPC although it did participate in the retention

scheme. Nonetheless, efforts to raise the quality and thus quantity of arabica

beans traded may open up new markets for robusta beans. Guatemala refused to

participate in either of the schemes for that reason. (Commodity Expert 17/05/01)

Guatemalan farmers suggested using their triage for industrial fuel or even

compost (Franklin 2001).

The Natural Resources Institute suggested several creative alternatives. NRI

claims that for every million bags of coffee removed from the global market

global prices will rise by two US cents per pound of coffee. Destruction of

low quality beans before they reach the market according to the NRI could improve

consumption by bettering quality. One means of disposal commercialised in Central

America is feeding the plant to cattle, goats and pigs, especially on small-scale

mixed crop-livestock farms where animal feed is frequently in short supply.

As mentioned previously, coffee plants can also serve as mulch to fertilize

land. Finally, although prohibitively costly, coffee beans could be made into

fuel briquettes-a widely used practice in Bangladesh according to one source

(OT Africa Line, Sept. 2001). Such briquettes could serve as a sorely needed

source of fuel in deforested areas. The prohibitive costs are incurred in transferring

the beans to the briquette manufacturing locations. Likewise and perhaps more

unrealistic at present--caffeine might one day be extracted from the husks of

the bean. (ibid.)

Product Differentiation

One means by which certain members of the coffee industry could help their

own corner of the market is through product differentiation. Colombia has been

most successful at creating a unique profile for itself as a high quality supplier

through the use of slogans such as "Juan Valdez" and "100% Columbian

Coffee"(Hamrlik, 2001). However the Colombian Coffee Federation was forced

to cut funding for its ad campaign nearly by 50% in the spring of 2001, due

to the drought and collapsed prices. More recently, another country has sought

to differentiate its own market. El Salvador is attempting to set itself apart

by emphasizing that 95% of its plantations harvest coffee under shade grown

conditions and 60% of the coffee cultivated land in El Salvador is planted with

gourmet Bourbon arabica beans (ProCafe, 2001). Potentially a country such as

Vietnam could do the same for itself by attempting to market high quality robusta

beans to garner a competitive advantage. New processing techniques are now available

that can take the bitter edge off the taste of robusta beans. In a frantic,

sleep deprived world, perhaps a new market could be carved out for the more

highly caffeinated robusta beans. However, such a campaign would do nothing

to quell the internal strife within the coffee industry. Thus it would make

little progress toward lifting the entire market up to a more stable state:

conducive to a sustainable existence for small farmers.

Sustainable Coffees (Fair Trade, Organic and Shade

Grown)

In order to protect both the farmers who grow coffee

and the environment in which coffee is grown three initiatives seek to ensure

that coffee production is more sustainable. So called, sustainable coffees:

namely fair trade, organic and shade grown have established or are in the process

of establishing a third party certification system to ensure that coffee is

grown under socially just conditions, free of chemicals or grown under a canopy

of trees that sustains biodiversity. Each certification system has a label indicating

to consumers that the coffee is grown under socially responsible and environmentally

sustainable conditions. What is certification?

The certification systems are a decentralized means

of monitoring the production of coffee internationally. They conform to the

stipulations of the World Trade Organization's Sanitaritary and Phytosanitary

Measures Agreement which state that

Member countries are encouraged to use international standards, guidelines

and recommendations where they exist. However, members may use measures which

result in higher standards if there is scientific justification. They can

also set higher standards based on appropriate assessment of risks so long

as the approach is consistent, not arbitrary. (WTO, 11/23/010)

Sustainable coffees defined:

Fair Trade coffee- purchase directly from cooperatives of small farmers

that are guaranteed a minimum contract price.

Organic coffee- produced with methods that preserve soil and prohibits

the use of synthetic materials.

Shade Grown coffee- grown in shaded forest settings and therefore supports

biodiversity and song birds in particular.

Fair trade, organic and shade grown certification intiatives set international

standards and guidelines by which coffee is grown more equitably and with fewer

pesticides that have been shown to have negative effects on the food chain,

the natural functioning of biomes, and on thus on human health. They are most

effective for coffee production in areas where plantations are small, cooperative

run endeavors, with funding for certification, which can be expensive. At present,

they are only being supported by the specialty coffee markets in consumer countries.

However the specialty coffee market in the United States is the largest in the

world, is growing by 5-10% per year, and controls 40% of national coffee sales

annually. To date these initiatives have focused on coffee production in Latin

America and on a limited basis in Africa. Organic, shade grown, and fair trade

coffee production have not reached much of Africa nor Southeast Asia, and their

dissemination may be hampered by the political situation in the producing country.

An essentially command controlled country like Vietnam, may not be conducive

to farmer owned cooperatives that sustainable coffee initiatives seek. Nevertheless,

they provide models for a more equitable and holistic trading system toward

which global trading systems should strive.

The Fair Trade Criteria

The fair trade initiative seeks to guarantee that coffee farmers are paid a

living wage in the local context. It fosters long term relationships between

importers, roasters, retailers, and the producing cooperatives.

(standards used by Transfair

USA and other members of the International umbrella group, Fairtrade

Labeling Organizations [FLO])

The

Organic Criteria:

Organic Production and Processing is based on a number of principles and ideas.

All are important and this list does not seek to establish any priority of importance.

- To produce sufficient quantities of nutritious wholesome, high quality

food.

- To work compatibly with natural cycles and living systems.

- To include the wider social and ecological impact within the organic production

and processing system.

- To enhance biological cycles by involving microorganisms, soil flora and

fauna, plants and animals within the farming system

- To encourage development of an ecologically valuable and sustainable aquatic

ecosystem.

- To maintain and increase long-term fertility and sustainability of soils

- To maintain, promote and increase agro-biological diversity through sustainable

production systems and protection of their ecological context.

- To maintain and promote genetic diversity by increasing the number of crop

and plant varieties and animal breeds in the farming system; including specific

attention to on-farm management of genetic resources.

- To promote the responsible use and conservation of water and water resources.

- To use, as far as possible, renewable resources in production and processing

systems

- To foster local and regional production and supply chains

- To create a harmonious balance between crop production and animal husbandry

- To g provide living conditions that allow animals to express the basic aspects

of their innate behaviour

- To minimise all forms of pollution

- To utilise biodegradable and recycled packaging materials.

- To produce durable, high quality textiles utilising ecologically sustainable

production and processing

- To allow and provide everyone involved with a quality of life to that satisfies

their basic needs, and furnishes an adequate return, within a safe, secure

and healthy working environment

- To support the establishment of an entire production, processing and distribution

chain which is both socially just and ecologically responsible

- To recognise the importance of, protect and learn from, indigenous knowledge

and traditional farming systems.

The Shade Grown Criteria:

Migratory songbirds are the motivational factor behind this sustainable coffee

initiative. By preserving the tree canopy in the Mesoamerican Biological Corridor,

the survival of nearly 150 songbirds is more secure. Little mention is made

of all of the other living species that are all conserved by protecting the

shade canopy, however that is an added benefit to shade grown coffee. Also,

Jorge Cuevas, owner of a farmers cooperative in Oaxaca, Mexico has said that

shade grown coffee is known to taste better since the cherries take longer to

develop(April 2001). A study conducted by the Commission for Environmental Cooperation

coaborated this fact, asserting that shade grown coffee typically grown at higher

elevations tends to a higher sugar content lending it a smoother, richer, better

taste. In addtion to its environmental and taste benefits, shade grown coffee

is healthier as it usually requires the use of less pesticides (CEC, 1999).The

criteria for shade grown coffee can be found at the Smithsonian Migratory Bird

Center website (click above).

The three sustainable initiatives are found together in select set of coffee

beans. Much discussion and thought is being put into triple certification of

coffee: fair trade, organic, and shade grown (London, 2001) . Fair trade coffee

frequently tends to be organic, but organic is not necessarily grown under fair

trade conditions. Arguments have been made that organic coffee may be more sustainable

as a cause coffee because consumers may grow fatigued with pity for farmers

sooner than they will cease to care about a product that is perceived to be

of higher quality as a result of being chemical free or grown under a canopy

(Hamrlik, 2001). In many cases, the sustainable coffees are not mutually exclusive

and by all accounts they set a precedent for a more equitable and sustainable

coffee market.

Agree [AGR] or Disagree [DIS] : AGR

Stage (ALLEGE, INPROG, or COMP): INPROG

6. Forum and Scope:

International Coffee Organization, International Fairtrade Labelling Organization,

and Mulitnational

7. Decision Breadth:

Potential number of countries affected: all coffee producing ~60 and

consuming countries.

8. Legal Standing:

Memorandum of Understanding (MOU)between trading partners--producer group cooperative

and importer/wholesaler/roaster/or retailer.

I. Within the WTO Appellate Body there are two "Pending Consultations"

related to coffee. They are "WT/DS209 European Commission- Measures Affecting

Soluble Coffee" and "WT/DS154 European Commission-Measures Affecting

Differential and Favorable Treatment of Coffee". Soluble coffee refers

to instant or freeze dried coffee. Both cases clearly relate to coffee and may

or may not be related to the purported "dumping" of coffee on the

market by Vietnam. But each case, should it reach the Active Panel stage and

the Appelllate Body and Panel Report Adopted stage will set legal precedents

with regard to the second most widely traded commodity in the world-coffee--in

international law as set by the WTO.

II. Vietnam's relatively recent admission into the WTO sparked a study by the

UNDP to assess the degree to which Vietnam is conforming to the Green and Amber

Boxes. It is entitled, "Overview of the Agricultural Sector in Vietnam:

Implications of the WTO Agreement on Agriculture". It concludes that Vietnam

has generally made great strides in transitioning from a centrally-planned to

a market-oriented economy over the last decade. Both Green (permissible subsidies)

and Amber (subsidies to be reduced) Box Domestic Support mechanisms in Vietnam

seem to be aligned with the WTO provisions. While its economy is in a stage

of transition and development, it has nonetheless reformed its agricultural

policies, especially those related to export management, according to international

rules and conventions. The report contends that the majority of future adjustments

related to Vietnam's WTO membership will deal with market access issues. The

greatest challenge Vietnam faces in negotiations with other WTO members, the

UNDP states, lie in the level of tariff concessions it concedes. With regard

to coffee, customs charges are levied that raise revenue for the Government,

and add to the Agricultural Price Stabilization Fund, renamed the Export Support

Fund. The fund "sets an extra fee on exported and imported goods that have

large differentials between local and export prices, or between local and import

prices, in order to stabilize domestic prices."(47) Such customs may violate

tariff binding provisions under the WTO. (http://www.undp.org.vn/projects/vie95024/agriculture.pdf

10-30-00)

IV. Geographic

Clusters

9. Geographic Locations

a. Geographic Domain: Asia

b. Geographic Site: Southeast Asia

c. Geographic Impact: Vietnam

10. Sub-National Factors:

No, however in Dak Lak Province, Vietnam--indigenous rights (see Other Cluster)

11. Type of Habitat:

TROPICAL [TROP]

V. Environment

Clusters

20. Environmental Problem Type:

Deforestation, pesticide pollution, biodiversity reduction, habitat loss

Logging and slash-and-burn agricultural practices contribute to deforestation

and soil degradation; water pollution and overfishing threaten marine life populations;

groundwater contamination limits potable water supply. (CIA, 2001)

The central highlands (where most of the coffee production takes place) contains

upwards of 42% of the nation's remaining forests (http://www.forestsandcommunities.org/Country_Profiles/Vietnam.html

21. Name, Type, and Diversity of

Species

Name: Grey-shanked Douc Langur (Pygathrix cinereus),

broad-leaved hardwood trees, bamboo, Elds Deer (Cervus eldi), Banteng (Bos banteng),

Douc Langer (Pygathrix nemaeus) and Concolor Gibbon (Hylobates concolor),Kouprey

(Bos sauveli)

Type: Large mammals, tree and other plant species

(including medicinal species), more than likely many other fungal and perhaps

bacterial species that might be useful to biological research and to the native

peoples according to their traditions.

Diversity: High degree of endemism

22. Resource Impact and Effect:

The production of coffee can be relatively environmentally friendly. Although

coffee plants produce the greatest quantity of beans in high sunlit conditions,

they produce more rich tasting beans under a shade canopy (Cuevas 2001). Unfortunately,

the production of robusta beans, the lower quality variety of coffee beans is

usually done in deforested areas in order to maximize the harvest by increasing

sun exposure. Vietnam, the foremost producer of robusta beans as of 2000, grows

the majority of its beans on recently denuded mountain slopes (Johnson 2001).

Within the last 50 years more than half of Vietnam's forests have been destroyed.

The following description of Vietnam's environmental degradation comes from

another TED case, vietwood

by Brian W. Hill.

Vietnam's forest cover has shrunk from 44 percent of the

country's

total land area in 1943 to 28 percent or 9.3 million hectares

today. During the Vietnam War, US military actions destroyed an

estimated 4.9 million hectares of forest cover. Currenty, the

country's remaining two million hectares of natural forests are

being reduced at a rate of 100,000 to 200,000 hectares per year.

Reforestation is not keeping pace with forest cover losses stemming

from unplanned agricultural clearances, forest fires, the

collection of firewood, and the harvesting of timber. If present

rates of deforestation continue, Vietnam's natural forests will

disappear by the first part of the next decade.

The Central Highlands were traditionally one of the most undisturbed areas

of Vietnam. But that is changing as coffee production increases in the area.

Nevertheless, the government has set aside Yok Don national park located in

the central highlands. It is the only protected example of Dry Dipterocarp forest

in Vietnam. The park has a total area of 60,000 hectares. Immediate threats

to biodiversity in the park include hunting, fire, encroachment and livestock

grazing. The park covers an extensive forest area estimated at over 400,000

hectares, some of which has been allocated to logging and surrounds the national

park. In addition the park is adjacent to intact forests on the western side

in Cambodia. This location holds potential for trans-boundary protection of

a large area, which is particularly important to the conservation of large mammals.

The park holds suitable habitat for the Kouprey (Bos sauveli) and local villagers

report its existence although scientific verification of such claims is pending.

Nevertheless, the Giant Muntjac (Megamuntiacus vuquangensis) is verfiably present

in the park and is hunted by villagers. Other rare species in the park include

Elds Deer (Cervus eldi), Banteng (Bos banteng), Douc Langer (Pygathrix nemaeus)

and Concolor Gibbon (Hylobates concolor). (Cuc Kiem Lam, http://www.undp.org.vn/projects/vie95g31/

Vietnam is sometimes compared to a dragon as it is a long, narrow country,

about 1700 km in length (with 3000 km of coastline). Temperate northern and

montane regions intersect with the tropical southern region. Vietnam's geography

is quite variable, including tropical rainforest, dry broadleaf deciduous forest,

marine coral formations and large inland rivers. Topography is built upon karst,

basalt, sandstone, as well as sand dunes. Such geographic an topographic variety

creates local isolation, which in turn has produced a patchwork of endemic species

(BAP, 1996). The areas of the greatest plant endemism include the Hoang Lien

Son range, the Central Highlands and Da Lat Plateau. The endemism of these areas

spans many vertebrate species such as birds, fresh water fish and mammals. According

to the Biodiversity Action Plan (BAP, 1996), Vietnam has a higher proportion

of endemic species than any of its neighbors in Southeast Asia.

The Vietnamese people depend heavily on this biodiversity. While their survival

is subject to sustained preservation of the forest, the poor local people seem

to have no choice except to exploit and so degrade forest resources. Today,

over one third of Vietnamese people - predominantly the ethnic majority 'Kinh'

people - depend on forest products.(Ngoc Thanh,

23. Urgency and Lifetime:

Low and Hundreds of years

24. Substitutes:Sustainable harvesting

of existent forest species, perhaps coupled with shade grown coffee. This will

improve the taste of the coffee while preserving the forest's biodiversity.

VI. Other

Factors

25. Culture:

Vietnamese Indigenous Turmoil

The government of Vietnam, with funding from large aid organizations such as

the World Bank, has invigorated the Vietnamese economy under the auspices of

its new economic plan begun in 1986 (Tran), doi moi, in part by redistributing

land to impoverished, landless farmers primarily from one ethnic class, the

Kinh. The Kinh people (the dominant ethnic class comprising most of the government)

have been encouraged to move from the North and the South to the provinces of

Dak Lak and Gia Lai in the central highlands. Until recently, the Kinh people

superstitiously avoided the central highlands and the area was thus left to

Vietnam's numerous hill tribes (Ksor Kok).

However, as a result of recent land distribution, deforestation and ethnic tension

have both been exacerbated. While the population of the central highlands area

experienced a 12% annual growth rate in the 1990s and the population doubled

to 1.9 million. Meanwhile the ethnic make up of Dac Lac has shifted from 50%

ethnic minority in 1975 to only 25% today. In February, masses of enraged highlanders

marched through Dac Lac and Gia Lai in protest of the arrests of two Jarai tribesman,

in the most dramatic show of unrest since 1997 when a thousand villagers protested

land distribution in the northern province of Thai Binh. Again in August, smaller

groups of hill tribe minorities burned two hectares of coffee plantations and

clashed with police as well as settlers. (Johnson 2001)

In the central highlands where 200,000 hectares of land are now covered with

abundantly fruitful coffee plants.. "The central highlands' troubles are

a microcosm of all the contentious issues facing Vietnam-land disputes, corruption,

a shaky economy and accusations of religious repression."(Johnson 2001)

Vietnam's deforestation begun in the war, continued with the search for fuelwood

and timber in the abject poverty that ensued, and is culminating with the country's

current economic thrust both to export coffee from the central highlands and

rice from the Mekong Delta (Oxfam). The rush to increase exports has created

extreme regional disparities within Vietnam and transformed its environmental,

ethnic, and economic geography. Nonetheless, the World Bank estimates that out

of its population of 70 million 80% are rural inhabitants and nine out of ten

are poor.

The ethnic tension in the central highlands of Vietnam is not likely to be

relaxed by the trends evident in the Vietnamese coffee labor force either. Over

the last nine years there has been a marked trend--farmers are getting paid

less and less for their work. Disputes over land tenure based on ethnic differences

are only exacerbated by mounting economic pressure. In December of 1991 farmers

were paid 26.2 cents per pound, while in December of 2000 they received 16.20

cents per pound. The labor market did fetch higher wages between 1994 and 1999,

but that trend seems to have reversed in the year 2000. (See Table 7)

Table 7. Prices paid to growers in exporting Member countries in US cents per

lb (Robusta): Vietnam

| |

Jan |

Feb |

Mar |

Apr |

May |

Jun |

Jul |

Aug |

Sep |

Oct |

Nov |

Dec |

| 1991 |

43.68 |

42.12 |

41.53 |

40.95 |

40.67 |

39.58 |

38.79 |

37.44 |

31.36 |

30.92 |

26.27 |

26.20 |

| 1992 |

28.11 |

32.38 |

29.75 |

29.77 |

30.28 |

29.93 |

30.85 |

31.16 |

32.36 |

30.92 |

26.27 |

26.20 |

| 1993 |

34.19 |

34.00 |

33.82 |

33.83 |

33.40 |

33.47 |

33.48 |

33.73 |

32.87 |

37.93 |

37.78 |

37.93 |

| 1994 |

38.13 |

46.14 |

4.41 |

47.90 |

72.42 |

91.18 |

119.99 |

126.94 |

116.83 |

118.47 |

113.56 |

99.14 |

| 1995 |

95.12 |

97.90 |

104.38 |

111.26 |

107.60 |

101.54 |

94.98 |

94.69 |

90.53 |

86.55 |

80.34 |

72.09 |

| 1996 |

59.72 |

67.96 |

70.02 |

70.02 |

72.09 |

65.89 |

57.64 |

58.85 |

49.36 |

45.09 |

36.08 |

40.64 |

| 1997 |

36.51 |

47.97 |

53.73 |

55.96 |

58.16 |

66.84 |

69.89 |

62.82 |

59.97 |

52.77 |

49.97 |

56.46 |

| 1998 |

67.54 |

64.68 |

67.45 |

69.87 |

78.61 |

77.21 |

58.65 |

57.03 |

61.98 |

61.98 |

60.75 |

61.59 |

| 1999 |

65.36 |

66.94 |

63.62 |

54.51 |

48.90 |

49.17 |

45.52 |

44.83 |

45.38 |

42.10 |

40.46 |

41.39 |

| 2000 |

35.51 |

33.89 |

31.61 |

30.00 |

29.01 |

28.34 |

27.04 |

25.09 |

24.03 |

20.59 |

17.21 |

16.20 |

Source: International Coffee Organization 11/15/01

http://www.ico.org/asp/statschoice2.htm

Global Social Implications in what used to be the second most prolific coffee

producing country:

Future disputes may be brought before the Appellate Board of the World Trade

Organization as a result of recent developments in Columbia. On Oct. 30, 2001

the Washington Post asserted that the critical state of the coffee commodity

market may be forcing some Columbian farmers to turn to coca farming in order

to support their basic needs. While Wilson cautiously reports, "Although

hard numbers are impossible to come by, evidence and informed estimates suggest

that only about 1,000 of the country's 560,000 coffee farms have scrapped coffee

plants in favor of coca or opium poppies," the coffee crisis is not expected

to lessen in severity any time soon. Thus the trend toward coca farming may

continue and gain strength in the coming years of tanked coffee commodity prices.

If so, it may be reasonable to expect that Columbia and perhaps Vietnam could

bring a case against developed countries under the auspices of the following

portion of the Agreement on Agriculture:

Having agreed that in implementing their commitments on market access, developed

country Members would take fully into account the particular needs and conditions

of developing country Members by providing for a greater improvement of opportunities

and terms of access for agricultural products of particular interest to these

Members, including the fullest liberalization of trade in tropical agricultural

products as agreed at the Mid-Term Review, and for products of particular

importance to the diversification of production from the growing of illicit

narcotic crops.

Perhaps a case could be constructed by a developing country Member against

a developed country Member or perhaps another developing country Member by utilizing

this provision of the Agreement on Agriculture. The state of the coffee commodities

market as a result of the glut on the market may be encouraging desperate farmers

to move toward the cultivation of illicit narcotic crops rather than diversifying

away from them.

http://www.ejil.org/journal/Vol9/No1/sr1e.html#TopOfPage

http://www.undp.org.vn/projects/vie95024/agriculture.pdf

26. Trans-Boundary Issues:

27. Rights: As is often

the case, when tensions rise internal fissures grow wider. The hill tribes of

Vietnam have suffered a long history of repression in Vietnam and Cambodia.

The French who colonized Vietnam from 1895-1954 labeled the hill tribes, the

montagnards or mountaineers because they have been marginalized to the highlands

by the dominant kinh people over centuries. While the Vietnamese government

regularly labels the same people comprised of forty distinct ethnic groups,

moi, or savages. The Montagnard Foundation has established its own website to

educate the world about what it claims are the abuses lobbied by the Vietnamese

government against the hill tribes or degar, meaning "sons of the mountains".

It states that coffee has sown "bitter seeds of hate" by encouraging

the government's torturing, repressing and persecuting (including sterilizing

women) the degar people. (Montagnard

Foundation) While such claims remain largely undocumented, Freedom House

has documented a governmental effort to crackdown on "banned evangelical

Christian 'house churches' that claim many minority converts". (Johnson

2001)

28. Relevant Literature

- Aguilar, Eloy O. "Ortega concedes defeat in Nicaragua's presidential

election." Managua, Nicaragua:Associated Press. Nov. 5, 2001.

- Biodiversity Action Planning Team (BAP). 1996. Biodiversity Action Plan

for Vietnam. Ministry of Science Technology and Environment, Hanoi.

- Bennett, Sara L. and Nguyen Thai Lai. "Water Quality Management in

Viet Nam." Reaching the Unreached--Challenges for the 21st Century, 22nd

Water Engineering and Development Center Conference. New Delhi, India. 1996,

p. 31.

- Collier, Robert. "International Prices are Low, Yielding Bonanza for

the Few," San Francisco Chronicle. May 20, 2001.

- "Columbia University Embraces Fair Trade Coffees From Green Mountain

Coffee Roasters." Yahoo! Finance. October 13, 2000.

- Commission for Environmental Cooperation. "Measuring Consumer Interest

in Mexican Shade-grown Coffee: An assessment of the Canadian, Mexican and

US Markets." Communications and Public Outreach Dept. of the CEC Secretariat,

October 1999.

- Commodity Expert. "APCP: Regional alienation rather than producer cooperation

main impression left by coffee retention talks." 17/05/01.

- Consumers' Choice Council. "Coffee Tasting Booklet" http://www.consumercouncil.org.

Nov. 7, 1997 09/03/01.

- Coote, Belinda with Caroline LeQuesne. The Trade Trap Poverty and the

Global Commodity Markets. Oxfam, 1996.

- Giovannucci, Daniele. "Sustainable Coffee Survey of the North American

Specialty Coffee Industry". Conducted for The Summit Foundation, The

Nature Conservancy, North American Commission for Environmental Cooperation,

Specialty Coffee Association of America, and the World Bank. May 2001. http://www.fairtradestudents.org.

November 13, 2001.

- Federal Agriculture Organization. "Coffee Commodity Notes." http://www.fao.org/waicent/faoinfo/economic/ESC/esce/cmr/cmrnotes/CMRcofe.htm

Feb. 2001. 10/13/01.

- Franklin, Stephen. "'Fair Trade' Coffee Perking Up Life." Chicago

Tribune. April 17, 2000. Business 4.

- Franklin, Stephen. "Coffee as Industrial Fuel Burning Issue for Growers."

Chicago Tribune. April 17, 2000. Business 4.

- International Coffee Organization, "Frosts and Droughts in Coffee Areas

in Brazil" http://www.ico.org/frosts.htm 12/17/01.

- Johnson, Kay "Brewing Discord: As coffee prices plunge, tension between

settlers and hill tribes is percolating in Vietnam' hills" Time Asia

April 2, 2001, Vol.157 No.13 http://www.time.com/time/asia/biz/magazine/0,9754,103845,00.html